Financial Planning is the process of incorporating all of your financial goals, aspirations and existing arrangements into one comprehensive approach

Financial Planning

Making sure you have the correct plans in place to minimise tax and give you the best chance of financial freedom in retirement

Retirement Planning

Should the worst happen you can be sure that your finances and loved ones are protected

Protection PlansWelcome to Hankley Financial Planning Limited

Based in Send, Surrey, Hankley Financial Planning is passionate about providing a high quality financial planning service.

The most common mistake we find individuals make in financial planning is not having a cohesive financial plan. Whilst most people have a variety of savings and investment products and an ideal for the future, they have not ensured that everything is working in harmony to achieve their goals. Allowing a single adviser, who you trust, to work with you to determine suitable financial decisions, will ensure that your aspirations can be met as efficiently as possible. We pride ourselves in translating even the most technical jargon into simple terms to ensure you understand the decisions you are making.

Why do I need Financial Planning Advice?

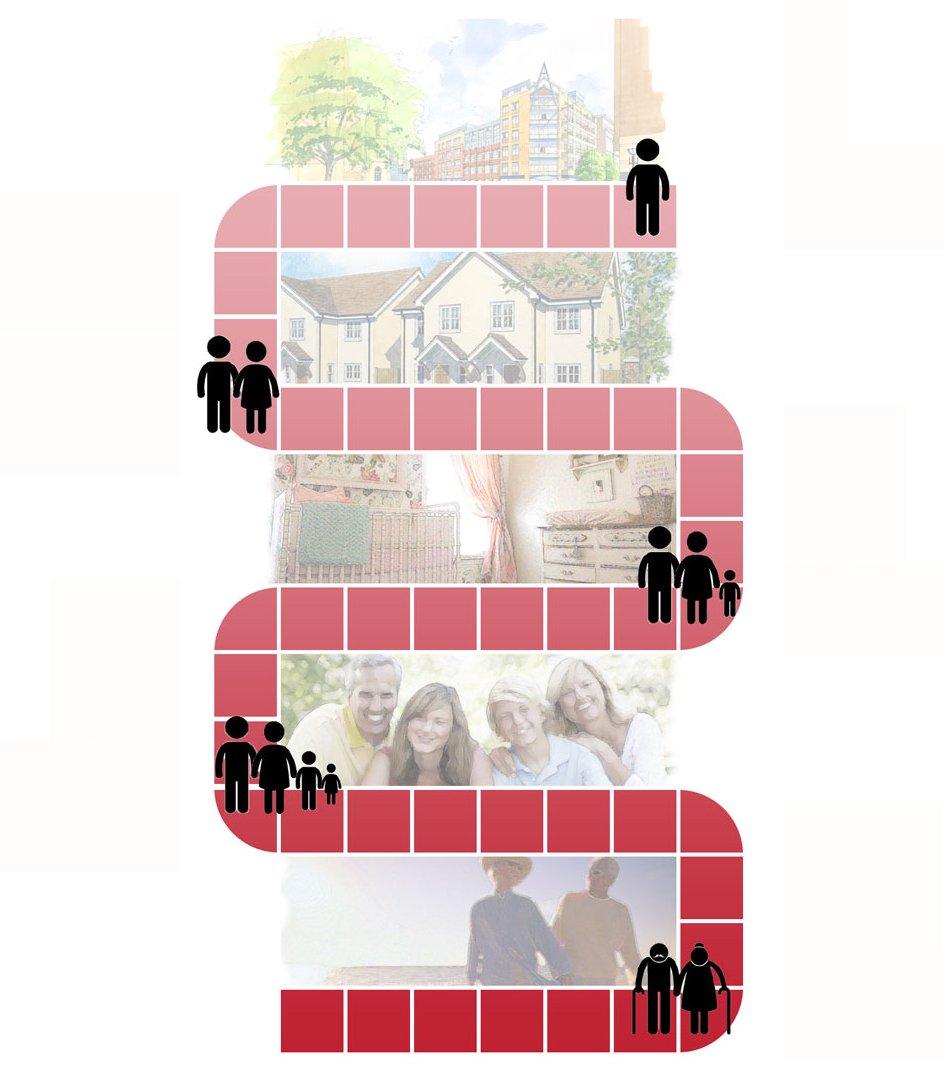

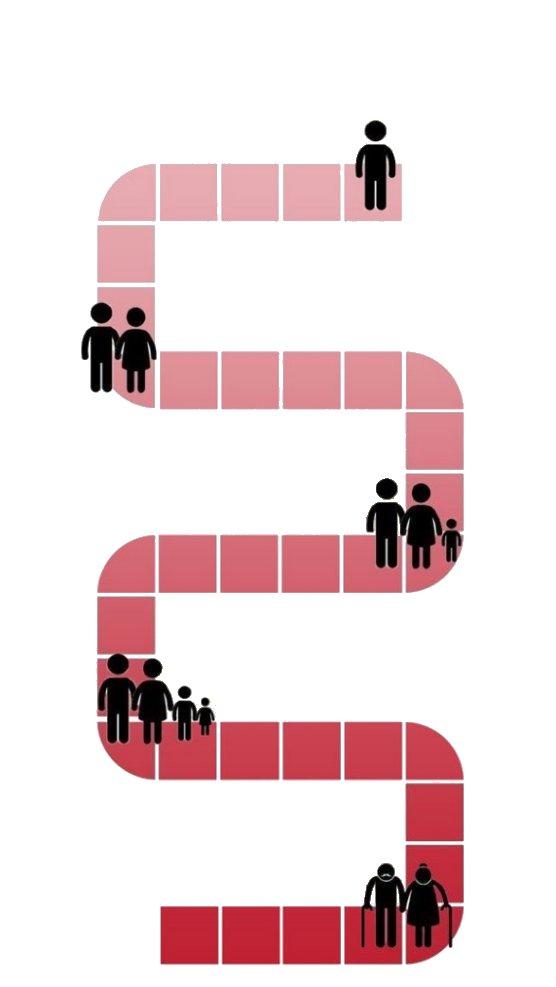

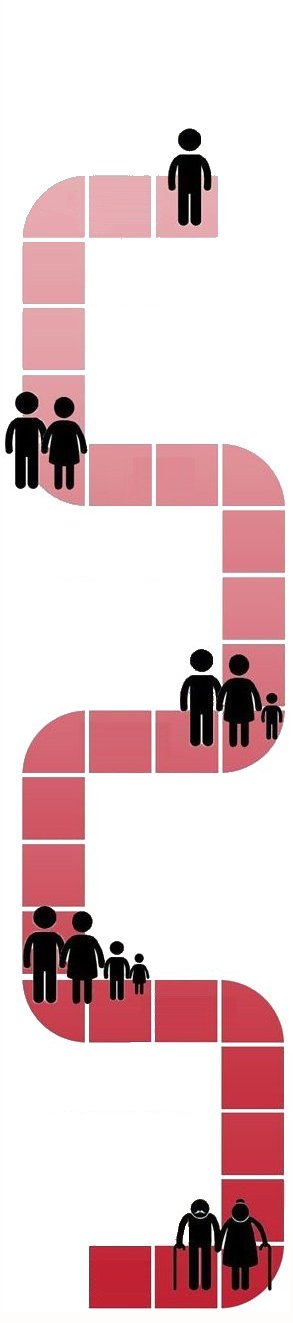

Here is also a point to consider....

In today’s terms, if you need £500,000 in your pension to provide an income of £25,000 per year at age 65, a basic rate tax payer would need to contribute £151.79 per month from the age of 20 (assuming a 6% growth rate). If you wait until age 30 to start your pension you need to contribute £289.79 per month to achieve the same outcome. That’s nearly twice as much....